Cash balance pension plans have seen a rebound in popularity as small businesses and professional groups seek a balance between sometimes competing desires to attract new employees, supplement benefits for senior executives and owners, and minimize tax and benefit expenses. Most often used as a complement to defined contribution arrangements such as 401k and profit sharing plans, properly designed cash balance plans provide a greater degree of flexibility and potentially much greater tax benefits. From both a short- and long-term standpoint, it may be an option worth exploring.

The trend towards seems to be irreversible. Employers continue to abandon the traditional defined benefit (DB) pension model, which pays retirees a certain pension for life, in favor of defined contribution (DC) plans, such as 401(k)’s, which are cheaper to set up and maintain, and which shift much of the funding burden and investment risk onto employees. According to the Investment Company Institute, total DC assets in the US grew to $8.2 trillion in the first quarter of 2019, 50% higher than their level at the end of 2012. While governmental entities have stuck more closely to the DB model, private sector DB pension plan assets have grown by only 15% over that same time period, to $3.2 trillion. As recently as 1991, private DB assets actually exceeded those held in DC plans.

Despite these trends, there are some downsides to the shift away from defined benefit plans. Many business owners participate alongside their employees in their company pension plans and would like to keep some of the advantages of the DB structure, not least of which is the greater potential for tax deductions and deferrals available in such plans. While most are happy with their relatively easy-to-administer 401(k) arrangements, some would like to supplement those plans with additional benefits to employees and themselves. Enter the cash balance pension plan. While DB plans in general are experiencing an outflow of assets, cash balance plans are thriving.

A cash balance pension plan is a type of DB plan that in some ways more closely resembles the DC model. Under a traditional defined benefit plan, assets are pooled within the plan for the benefit of all plan participants, and funding levels are calculated according to the total accumulated assets and benefit obligations for all participants on an aggregate basis at a given point in time. Cash balance plans, on the other hand, create hypothetical1 segregated accounts for each plan participant, wherein annual credits are accumulated to determine a ‘cash balance’, assigned for the benefit of each participant. These annual credits take the form of both a) “pay credits” (employer contributions), which are typically based on a certain formula applied to each participant’s annual salary, and b) “interest credits”, which are determined by applying a specified fixed or variable interest rate to any existing balance in an account. At such time as the participant separates from service, either due to retirement or other change in employment, the vested portion of that accumulated cash balance may be paid out as a lump sum or annuitized as an income stream over a specified period or lifetime.

For example, under a typical cash balance pension, the plan may call for each employee to be credited with an annual employer contribution of 5% of salary. An employee earning $50,000 per year would result in a credit of $2,500. Now suppose that that same plan’s specified interest crediting rate was equivalent to that year’s average 30-year Treasury bond yield, which for a particular year might be, say, 4%. This means that if the participant’s previously accrued cash balance in the account was $200,000, she would be credited with an additional $8,000 (200k x 4%), which when added to the employer contribution calculated above would result in her new cash balance of $210,500.2

The major selling point of cash balance plans for business owners trying to optimize their employee benefit programs, however, is the opportunity to both a) realize greater tax savings to the business from higher contribution limits and b) receive a proportionately greater share of the retirement benefits accruing from such plans. For example, a plan could be set up so as to assign different contribution levels based upon different participant classifications, such as ownership status, compensation level, and years of service. Note that these terms must meet IRS non-discrimination restrictions. However, companies can combine the cash balance plan with a defined contribution plan in such a way that these requirements are met while still maximizing the benefit to their owners.

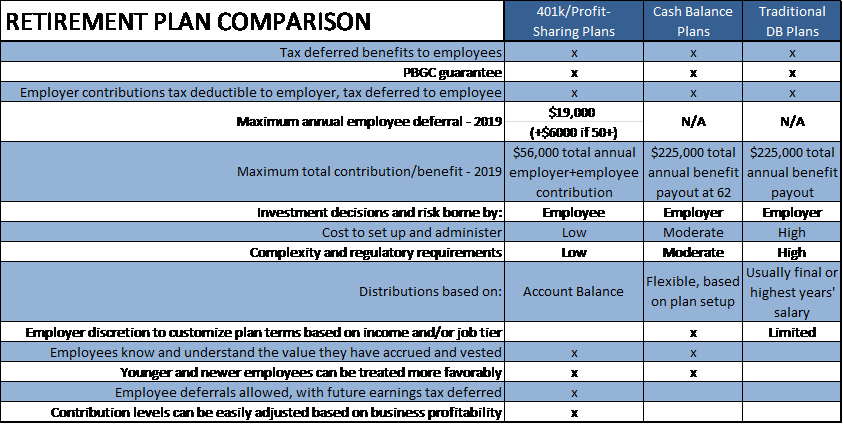

These annual contributions (and tax deductions) can be significant ($200,000 or more, depending on the plan and the ages and incomes of participants). There is no annual contribution limit to a cash balance plan, whereas each participant’s limit on employee deferrals and employer contributions to DC plans is $56,000 for 2019. The only limitation to a cash balance plan is a $225,000 maximum benefit limit (for 2019) based on an equivalent annuity taken at age 62 (equivalent to a $2.8 million lump sum). In addition to the tax deduction received on contributions, recent tax reform provides for a 20% deduction on qualified business income below $415,000 for certain professional trades and businesses. If a cash balance plan can be implemented so as to bring pass-through income below that threshold and thereby qualify for that deduction, the incremental tax savings increases exponentially.

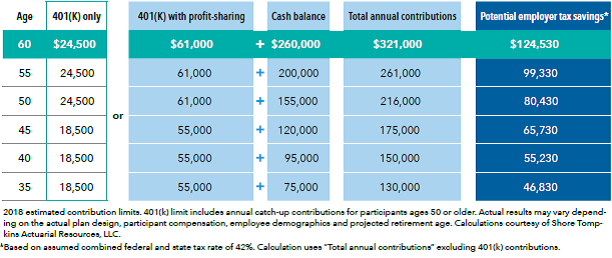

These types of plans are especially popular with medical and other professional groups where the earnings and tenure of the principal owners tend to be higher than other employees. Furthermore, the choice is not either/or; cash balance plans work particularly well when paired with defined contribution (401k, profit-sharing) type plans. The following table from Capital Ideas provides a visual example of how these owners might take advantage of these tax benefits while also receiving a proportionally greater share of the retirement benefits relative to his presumably younger employees.

Implementing a cash balance pension plan which optimizes its benefits while ensuring compliance with ERISA and IRS requirements can be a moderately complex process, requiring coordination of accountants, plan administrators, and investment managers. We at Olson Wealth Group can help lead you through the process, and match you up with our network of experienced, reliable professionals.

Here is a recap of the distinct features of a cash balance pension plan:

Olson Wealth Group is a full service wealth management firm. With wise counsel and clear strategies, our experienced specialists provide tailored approaches that strive to maximize wealth. For more information, please visit OlsonWealthGroup.com

A Cash Balance plan may be appropriate for businesses with consistent revenues for long-term funding where owners are older and earn more than the average employee. These types of plans have additional costs and generally involve engagement of an actuarial firm for plan administration. Traditional 401(k) plans are employee-funded and allow for optional employer contribution; employees can defer up to $19,000/yr. (additional catch-up contributions of $6,000 if age 50 or older), with total combined contributions not to exceed $56,000/yr. Profit Sharing Plans are employer-funded and allow contributions to vary from year to-year depending on profitability. Cash Balance Plans must be amended in order to change contribution levels. Traditional 401(k) and Profit Sharing Plan distributions taken prior to age 59 ½ (age 55 if separated from service), may be subject to 10% penalty tax, in addition to ordinary income tax, and minimum distributions may be required at 70½ . Cash balance plan participants are eligible to receive the vested portion of their account balances when they terminate employment. This information was developed as a general guide to educate plan sponsors, but is not intended as authoritative guidance or tax or legal advice. Each plan has unique requirements, and you should consult your attorney or tax advisor for guidance on your specific situation. In no way does advisor assure that, by using the information provided, plan sponsor will be in compliance with ERISA regulations.